Getting a mortgage on a property with subsidence may deter certain lenders, but there are still a range of options open to you, particularly with the help of a specialist mortgage advisor.

Before you begin, understanding exactly what subsidence is, what causes it and the effects it can have on a property enables you to make a better and more informed purchasing decision.

Can you get a mortgage on a house with subsidence?

Yes, you can get a mortgage on a house with subsidence issues, but there may be some extra snags during the process of buying, as well as potential problems down the line.

You’ll first need to establish the extent of historic subsidence issues so that you can discuss this with potential lenders.

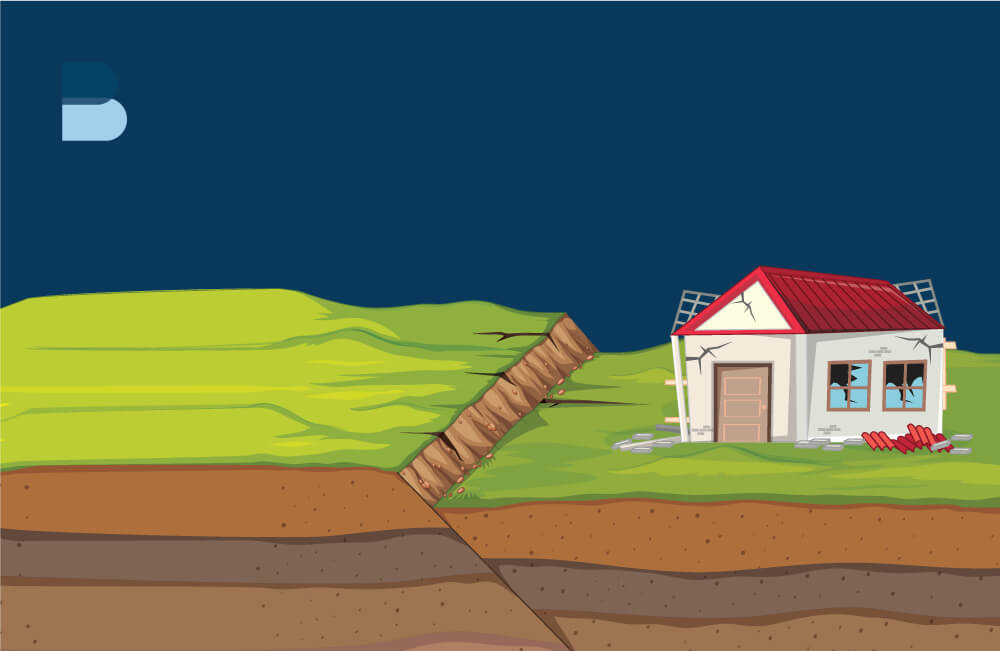

What is subsidence?

Subsidence refers to the downward movement or ‘sinking’ of the Earth’s surface or ground supporting a structure. There are a number of possible causes for subsidence, but it generally results in structural instability, cracks and jammed doors/windows.

In some cases, it’s severe enough to cause noticeably uneven floors and surfaces within a property.

What causes subsidence?

")

Subsidence can be caused by a variety of factors, ranging from soil losing moisture and shrinking, to mining and excavation causing underground voids to collapse:

- Clay soil shrinkage - During dry weather, soil which is rich in clay dries out and contracts, which can lead to subsidence.

- Vegetation/trees - Roots absorbing moisture from soil underneath a property can lead to shrinkage.

- Leaking drains/water mains - Large water leaks can dislodge and wash soil away beneath the foundations of a property.

- Mining and excavation - Whilst uncommon, underground mines or excavations can collapse and cause a knock-on effect on the ground above.

- Underground fluid extraction - If oil or natural gas is extracted/released from pockets below the surface, surface land can sink.

How does subsidence affect properties?

Subsidence causes the uneven shifting or sinking of property foundations. One way in which this can affect properties is by causing structural damage such as diagonal cracks, particularly near windows and doors.

Subsidence usually also causes a property to lean or sink partially, which has further effects like jammed doors and windows, resulting from distorted or compressed frames.

In extreme cases, subsidence can even result in significant structural damage, where extensions or conservatories break away from the main house structure.

Ongoing vs historic subsidence and the impact on getting a mortgage

If the property you’re looking at has historic subsidence issues which are no longer actively causing trouble (usually because of actions such as underpinning), it is usually regarded as highly mortgageable, but will require specific documentation to prove issues have been addressed, and aren’t going to reappear.

Most lenders will conduct or require a thorough survey of the property, a ‘certificate of structural adequacy’ and guarantee for any repair or maintenance work done to amend the issue.

If the issue is ongoing, your mortgage options become much more limited. This is when the ground is still actively moving and causing further issues. Your main option in this case is seeking a specialist lender through a mortgage broker, who is prepared to negotiate this risk with you.

Lending criteria for properties with subsidence or underpinning

")

Many lenders will approve mortgages for properties with past subsidence or underpinning, though there are generally certain criteria which need to be met:

- Structural engineers report - Most lenders require a report stating the cause of the subsidence has been removed or amended.

- Certificate of structural adequacy - Essential to prove that work has been signed off and the property is structurally sound.

- Repair guarantees - For repair or maintenance work, such as underpinning, you’ll usually need a 10 year and insurance-backed guarantee.

- Insurance - The property must be fully insurable, often with specialised policies for recent subsidence history.

Does a mortgage valuation check for subsidence?

A basic mortgage valuation check does not specifically check for subsidence, though it may uncover serious issues.

Standard valuations are usually brief and therefore won’t reveal underlying structural problems, unless they were already visible and obvious to the human eye.

Does subsidence affect the value of a property?

(1)")

Subsidence can drastically impact property value, depending on how severe it is. Generally, the structural risks caused by subsidence are enough to decrease property value by 20 - 25%, though more extreme cases will decrease value even more.

This is the case even for many underpinned properties, due to the stigma, insurance needs and increased risks associated with such properties.

Can you get a mortgage on a property with minor subsidence?

You can usually get a mortgage on a property with minor subsidence, particularly through specialist lenders or an experienced local broker such as Barlow Irvin.

Lenders will usually ask for proof that the issue is resolved to a professional standard.

Can you remortgage a property with subsidence?

You can remortgage a property with subsidence, but we’d recommend that you assess your options carefully before making any decisions.

Remortgaging with a new lender would mean you are treated as a new customer, so you’d have to manage the subsidence and required documentation from scratch again.

The other option would be a product transfer under the same lender, but you may have to prove work done to rectify subsidence in this case too.

To discuss your options, get in touch with Barlow Irvin financial advisors.